31 July 2023

Cautious optimism’ as equity release activity picks up at the end of Q2

Equity Release Council: Q2 2023 equity release market statistics

- Summary

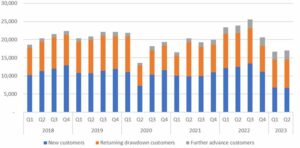

- The number of active customers in Q2 rose slightly to 17,028, up 2% from the previous quarter, despite remaining 29% down year-on-year.

- Total lending of £664m was down 5% from the previous quarter, making it the quietest since Q3 2016 (£571m) for lending.

- New customers increasingly opt for drawdown lifetime mortgages over lump sums compared with 12 months ago.

- At £59,294, the average first instalment from a new drawdown plan was 35% lower than a year ago (£90,646 in Q2 2022) and the smallest since Q1 2017

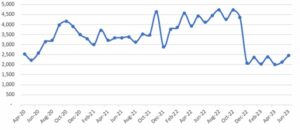

- April was the quietest month of Q2, with the number of new plans picking up in May and again in June as monthly activity reached its highest point of the year-to-date.

David Burrowes, Chair of the Equity Release Council, comments: “Higher interest rates have inevitably had a significant impact on the demand for lifetime mortgages like other mortgages, but the gap between residential and lifetime mortgage rates has narrowed over the last year.1 Equity release remains competitive and has lost none of the extra protections that have been added in recent years.

“Innovations in equity release can come into their own in a higher rate environment, with drawdowns allowing customers to take what they need in the short-term and make extra withdrawals in future if their circumstances change and interest rates fall. Optional repayments also give people freedom to keep their borrowing under control by limiting the effect of compound interest.

“The socio-economic factors for releasing equity remain. People are living longer, they are not saving enough for retirement and they want to help themselves and their loved ones to live more comfortable lives. We have seen steady growth in new customer activity in Q2, with June the busiest month of the year so far. While it is too early to call this as the start of the recovery, there is cause for cautious optimism and we remain confident in the strength of the market.

“Financial and legal advice remain vitally important to help customers understand their options. Equity release products are crucial in helping to meet current needs and avoid a later life lending drought, with higher interest rates and affordability tests making capital repayment or interest-only options harder for older borrowers to access.”

2.Key statistics for Q2 2023

Overall activity

- A total of 17,028 new and returning customers used equity release products between April and June 2023 to unlock wealth from their homes. All new customers can benefit from being able to make penalty free partial repayments in future to reduce the effect of compound interest, without any obligation to repay the loan plus interest until they pass away or move into long term care.

- The number of active customers this quarter was down 29% year-on-year from 23,910 in Q2 2022, although there was a slight increase (2%) from 16,691 in Q1 2023.

- A total of £664m was unlocked by new and returning customers between April and June. This represents a fall of 5% on the previous quarter (£699m) and makes Q2 2023 the quietest lending period by this measure since Q3 2016 when £572m was accessed.

Trends among new customers

- The number of new plans agreed for Q2 2023 was 6,682 down by 1% from 6,766 in the previous quarter and down 46% on an annual basis compared to Q2 2022 when 12,485 new plans were taken out.

- New customer numbers fell to 2,004 in April from 2,384 in March, before recovering in May and June to 2,117 and 2,462 respectively. The uptick towards the end of the quarter suggests a level of certainty returning to the market, despite wider mortgage rate trends.

- New customers were broadly split when it comes to product choice: 52% opted for drawdown lifetime mortgages, taking an initial withdrawal up-front with more held in reserve for future use, while 48% of customers opted for a single lump sum. One year ago in Q2 2022, the equivalent split was 45% drawdown and 55% lump sum.

- The higher interest rate environment, coupled with lower maximum product loan-to-values (LTV) available, has seen customers reduce the amount they borrow. At £59,294, the average first withdrawal from a new drawdown plan represents a 35% decrease year-on-year from £90,646 in Q2 2022 and is the smallest amount seen since Q1 2017. This is despite UK house prices having risen by a third (33%) since March 2017.2

- Having reduced their total loan sizes by 21% over the last year from £137,480 to £108,645 over the last year, new drawdown customers are now taking 55% of this sum up-front and saving the rest for future use, compared with taking 65% up-front in Q2 2022.

- The average size of a new lump sum lifetime mortgage reduced by 29% year-on-year, with customers taking £94,266 between April and June compared to £132,331 a year earlier. This is the lowest amount since Q2 2019 (£93,712).

Trends among returning customers

- With interest rates fixed or capped at the point of withdrawal for products which meet Equity Release Council standards, the number of drawdown customers making new withdrawals from existing loans rose marginally by 1% in Q2 2023 compared to Q1 2023.

- However, the number of returning drawdown customers fell by 16% compared with Q2 2022, from 9,305 to 7,817.

- Returning customers reduced their borrowing in Q2 compared to the previous quarter with the average returning drawdown customer taking £12,468 from their agreed reserves. This was 7% less than Q1 2023, and 8% less than in Q2 2022 when the average drawdown was £13,506.

- The number of further advances (loan extensions) agreed on existing plans increased on the previous quarter, up 15% from 2,193 in Q1 2023 to 2,529 in Q2 2023. This is also a 19% rise compared to a year ago. This may be a sign of historic customers needing more funds in the current climate and finding their available equity has grown following recent house price gains.

Details of equity release products and pricing for Q2 are available via the Spring 2023 Market Report

3.Market data

Graph 1: Equity release customers numbers, by type of customer, Q1 2018 to Q2 2023

Graph 2: Number of new equity release plans agreed per month, April 2020 to June 2023

Source: Equity Release Council

4.About the data

The Equity Release Council’s market statistics are compiled from member activity, including all national providers in the equity release market. This latest edition was produced in July 2023 using data from customer activity during the second quarter of the year (April to June). All figures quoted are aggregated for the whole market and do not represent the business of individual member firms.

Equity release products are available to homeowners aged 55+, enabling them to release money from the value of their home following a regulated process of financial advice and independent legal advice to determine whether this is suitable for their individual circumstances and long-term needs. Funds released are typically used for a range of purposes including providing additional retirement income, funding one-off expenses and lifestyle purchases, consolidating debts, meeting homecare costs and gifting a ‘living inheritance’ to family or friends.

For a comprehensive list of members, please visit the Council’s online member directory.

1 Moneyfacts UK Mortgage Trends Treasury Report shows the average 2 year-fixed rate across all LTVs rose from 2.86% in April 2022 to 5.35% in April 2023 (+2.49), while the average 5-year fixed rate rose from 3.01% to 5.05% (+2.04). Over the same period, Equity Release Council analysis of Moneyfacts data shows the average equity release rate rose from 4.75% to 6.20% (+1.45).

2 Office for National Statistics, UK House Price Index, May 2023, showing a 30% increase in average UK house prices from £215,236 in March 2017 to £286,000 in May 2023

5. About the Equity Release Council

The Equity Release Council is the representative trade body for the UK equity release sector with more than 750 member firms and 1,900 individuals registered, including providers, funders, regulated financial advisers, solicitors, surveyors and other professionals. It leads a consumer-focused UK based equity release market by setting authoritative standards and safeguards for the trusted provision of advice and products. Since 1991, more than 650,000 homeowners have accessed £46bn of property wealth via Council members to support their finances. The Council also works with government, voluntary and public sectors, and regulatory, consumer and professional bodies to inform and influence debate about the use of housing wealth in later life and retirement planning.

For more information:

Visit www.equityreleasecouncil.com

Email Instinctif Partners at [email protected]

Phone Jamie Till and Libby Wallis on +44 (0) 207 457 2020

Share this post