Equity Release Market Records 10% Year-on-Year Growth Driven by New Customer Borrowing

| Overall activity – Q2 2025 | Quarterly change | Annual change | |

| Total lending | £636m | -4% | +10% |

| Total plans | 14,404 | 0% | +1% |

| New plans | 5,319 | 0% | +2% |

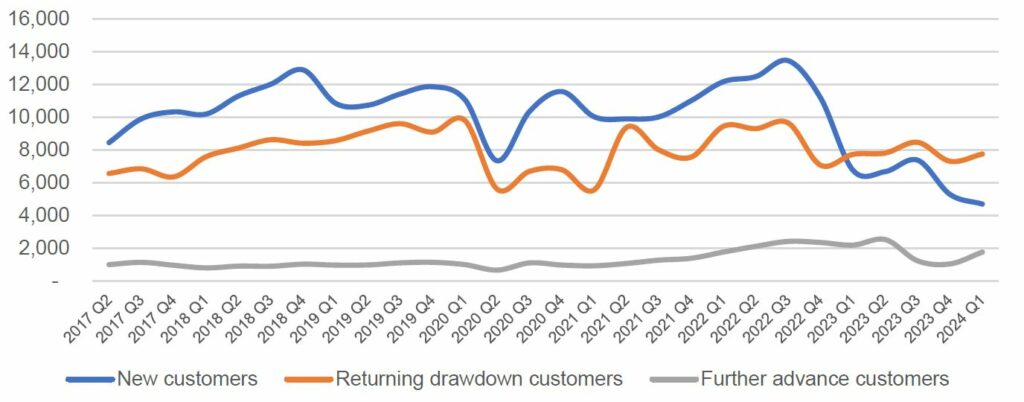

| Returning drawdowns | 7,640 | -1% | -5% |

| Further advances | 1,445 | +9% | +40% |

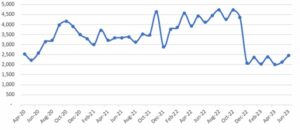

Older homeowners unlocked £636 million in property wealth with 14,404 new and returning customers in Q2 2025, as the equity release market continued its year-on-year growth, according to the Equity Release Council’s latest quarterly market report.

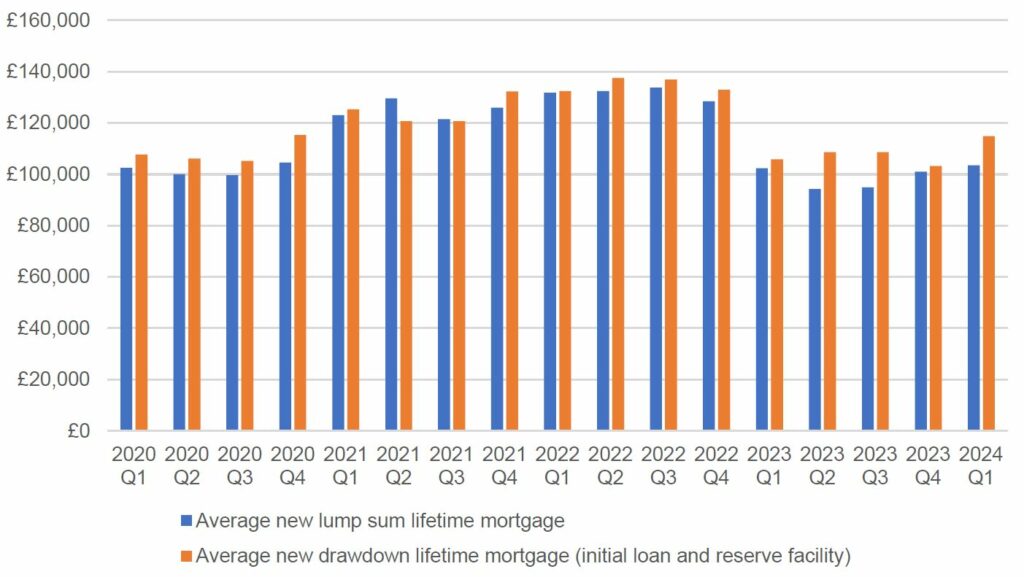

This is a 10% increase in total lending when compared to Q2 2024 (£578m) and was driven by new lump sum mortgage customers taking on average £126,422 or 14% more than in Q2 2024 (£110,969).

That said, the figures did highlight a 4% quarter on quarter drop in lending as borrowing in this sector mirrored challenges seen in the residential mortgage market due to ongoing economic uncertainty, changes to Stamp Duty and the later Easter holidays.

The number of plans taken out remained static quarter on quarter, but there was a slight increase in the volume of new plans (+2%) and total plans (+1%), when compared to 2024.

Further advances – which make up less than 7% of the total amount borrowed – saw a 40% year on year increase in plans as existing customers chose to take advantage of house price increases and additional product flexibilities to borrow more.

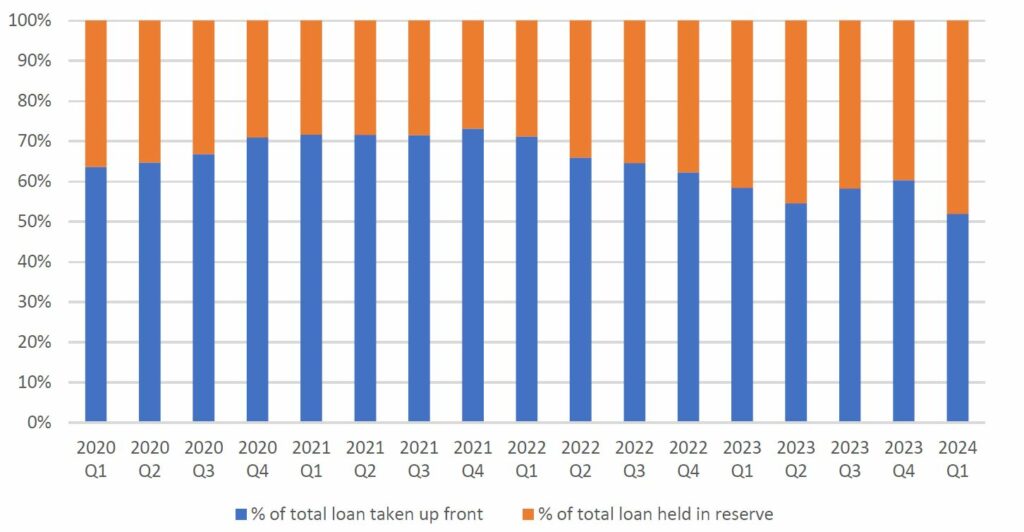

The relative importance of flexibility was highlighted further with 55% of customers in Q2 2025 deciding on drawdown products which allow homeowners to release an initial amount (Q2 2025 – £65,856) and agree a reserve facility (Q2 2025 – av. £53,338) for future use.

While product availability remained robust with over 1,669 plans for advisers to choose from at the end of June, the average APR was 7.24% in Q2 2025. This is higher than in Q2 2024 (6.64%) as gilt yields continued to rise as investors look for guaranteed returns amid global economic uncertainty.

| Average loan sizes | Quarterly change | Annual change | ||

| New lump sum | £126,422 | -1% | +14% | |

| New initial drawdown | £65,856 | -6% | +1% | |

| New drawdown reserve facility | £53,338 | -13% | +16% | |

| Returning drawdown | £13,150 | -5% | +4% | |

| Lump sum further advance* | £30,180 | -7% | +7% | |

| DD initial further advance* | £27,303 | +1% | +2% | |

| DD further advance reserve facility* | £6,545 | -3% | -21% | |

| Product choice among new customers | Drawdown: 56% | Lump sum: 44% | ||

| * = the number of customers taking further advances are very low so the figures are highly volatile. | ||||

The Council’s data is unique in that it is made up of aggregated figures collected from all UK equity release providers, encompassing business from advice firms across the market.

Commenting on the data, David Burrowes, Chair of the Equity Release Council, said:

Today’s figures show a resilient equity release sector which despite challenging economic headwinds, has recorded 10% year on year growth in borrowing with the total amount released in Q2 2025 reaching £636m. Growth which continues to be driven by new borrowers accessing greater amounts of housing equity to manage debt, boost income and support their wider families.

“While the equity release market face some of the same challenges seen in the residential mortgage market, new lump sum and drawdown loans are up as customers take advantage of stable long-term house price growth to support their later life finances. An approach which is only likely to grow in the future with Fairer Finance predicting that by 2040, over half of UK households (51%) are expected to require housing wealth to support their spending needs in later life and retirement.

“The Later life lending market will inevitably grow as more customers look to their housing wealth to boost retirement income and meet care needs. We need to be ready and resilient to build upon strong advice standards, product innovation and a commitment to support a wider range of customers as this provides significant opportunities for the market.

“We look forward to making the most of the opportunity presented by the recently launched FCA discussion paper into the ‘Future of the Mortgage Market’ which recognises the significant role of housing wealth in paying for retirement and that flexible lifetime mortgage products for older consumers are becoming ‘increasingly mainstream’.”

ENDS

To read the full report click here.

About the data:

The Council’s market data is compiled from actual whole-of-market returns and is not estimated nor grossed up, making it the UK’s definitive equity release data. All data has been collated by the Council, unless otherwise stated.

About the product: Equity release allows older people to access the wealth in their homes, without necessarily having to sell or move. Lifetime mortgages make up more than 99% of the market. They enable people to borrow against their homes without making repayments unless they choose to. The loan and interest, or part thereof, is paid when the customer dies or goes into long term care. Since 1991, more than 950,000 homeowners have accessed £50bn of property wealth via Council members to support their finances.

About the Council: The Council is the representative trade body for the UK equity release market. Plans that meet the Council’s standards come with six product safeguards: no negative equity guarantee; fixed or capped rates for life; secure tenure for life; the right to port; the right to make overpayments and no early repayment charge if you move into care provided a medical certificate is provided. In the UK, these safeguards are underpinned by mandatory independent legal advice, which ensures the customer understands the risks and implications of the plan.

More information: Visit www.equityreleasecouncil.com; call Lee Blackwell, Director of Communications and Marketing at the Equity Release Council on 07950798072; email [email protected]